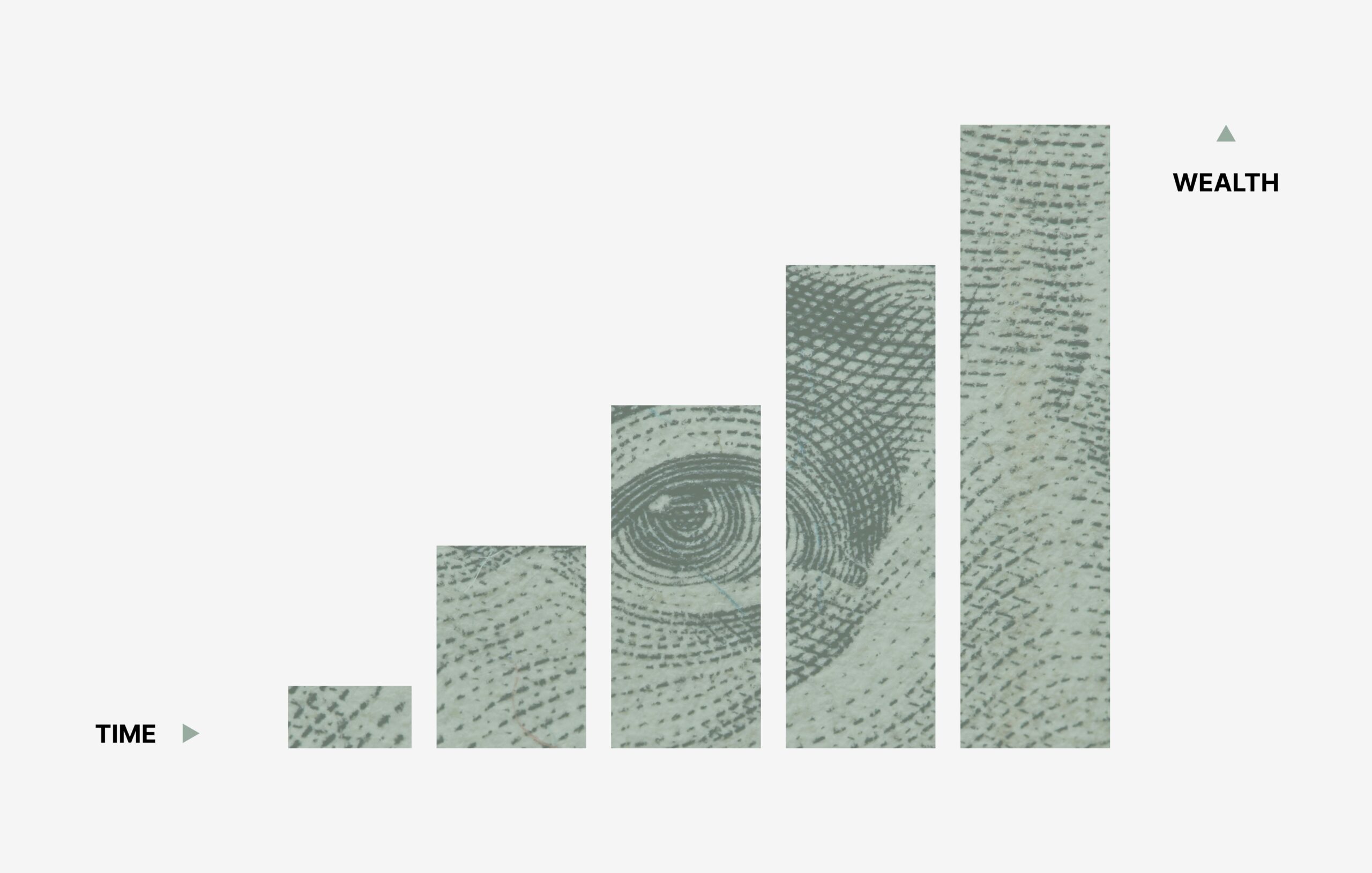

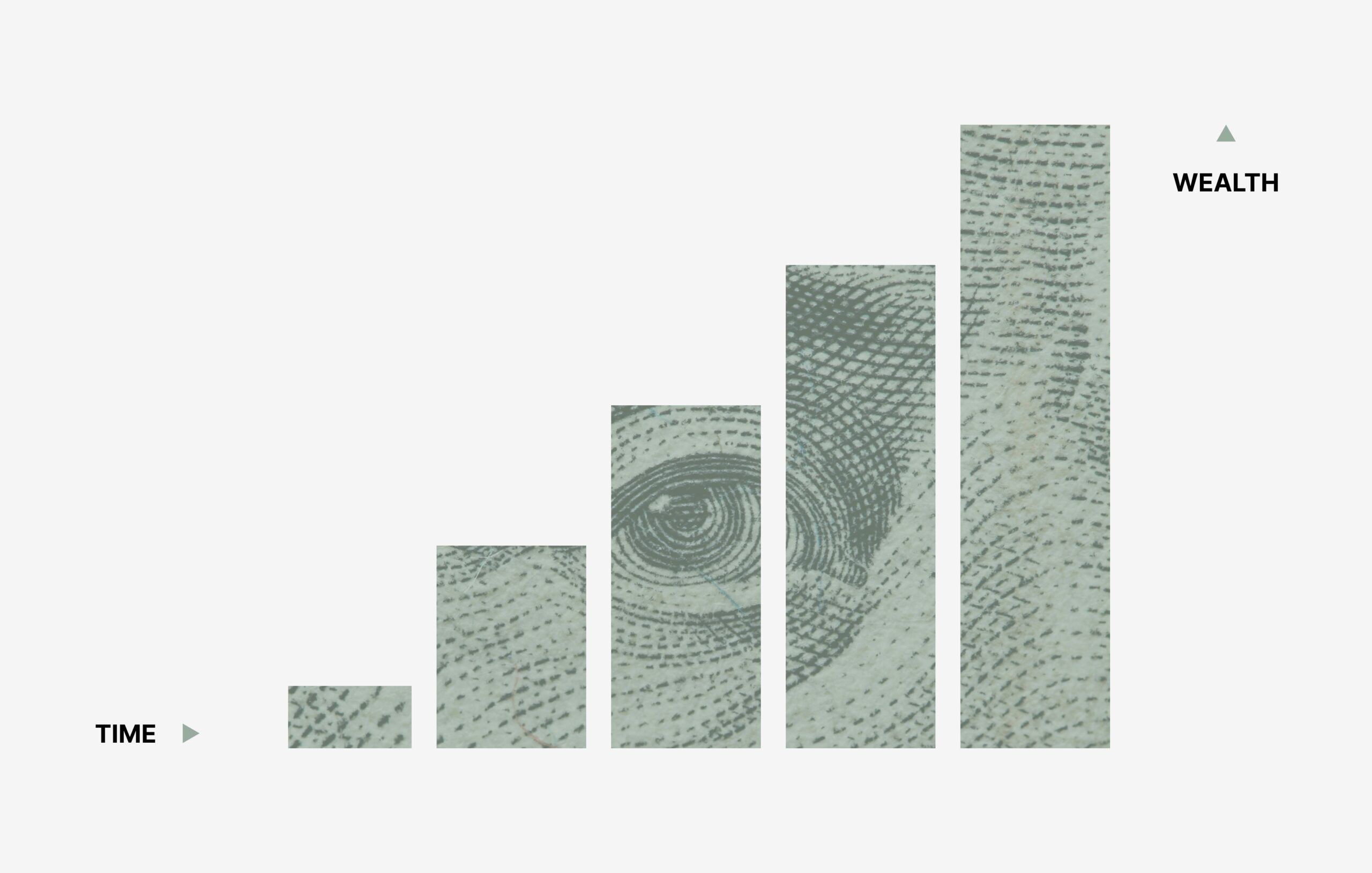

Understanding the 1% Wealth Shift

The 1% wealth shift refers to the continuing trend of wealth concentration, where a disproportionately small segment of the population amasses a significant portion of the total wealth. This phenomenon has resulted in an increasing gap between the affluent and the working or middle class, raising concerns about economic equity and social stability. Factors contributing to this wealth shift include various economic trends, globalization, and rapid technological advancements, all of which play critical roles in shaping the contemporary financial landscape.

Economic trends such as inflation, wage stagnation, and the rising cost of living have disproportionately affected the average citizen while enabling wealth accumulation for those already privileged. For instance, while salaries for many have remained stagnant over the past few decades, asset prices in property and the stock market have surged, favoring those with existing wealth who can invest. This has created a situation where the rich get richer, further exacerbating income inequality and limiting upward mobility.

Globalization has also significantly impacted wealth distribution, as it has facilitated capital movement and labor outsourcing, resulting in job losses in some sectors. While globalization creates new markets and opportunities for businesses, it often does not translate into equitable access for all socio-economic classes. Certain industries thrive globally, disproportionately benefitting those individuals who have the resources and skills to adapt to this new environment.

Additionally, technological advancements, particularly in automation and the digital economy, have transformed industries and labor markets, often displacing lower-income workers and disproportionately benefiting those with technological expertise and investments. This shift toward automation has led to job polarization, where high-skill and low-skill jobs increase, while middle-skill jobs dwindle, thus widening the wealth gap.

By examining the statistics and insights from economic experts, it becomes clear that the 1% wealth shift poses serious implications for financial security and social cohesion. Understanding the mechanics of this transformation is essential for grasping its effects on society as a whole.

The Power of Small Changes in Wealth Management

Wealth management often brings to mind complex strategies and substantial investments; however, the journey to financial security can begin with small but impactful changes. Individuals willing to alter their financial habits can significantly improve their overall wealth and achieve long-lasting security. The principle of making small adjustments is rooted in the notion that every little bit counts and, when compounded over time, can yield considerable results.

One practical approach to initiating small changes is through effective budgeting. By tracking income and expenses diligently, individuals can identify unnecessary outflows. Simple actions, such as reducing impulse purchases or reallocating funds to necessary categories, can lead to increased savings. For instance, a family that commits to cutting back on dining out just twice a month can redirect that money into a savings account or an investment vehicle, thus facilitating wealth accumulation over the long term.

Saving is another critical element of wealth management that can be improved through minor adjustments. Establishing an automatic saving plan, even if it’s a small percentage of your income, can create a significant financial buffer over time. Consider individuals who have managed to save for emergencies or investments by automatically transferring a portion of their paycheck into a separate account—this small, consistent action fosters discipline and can lead to greater financial security.

Investing, too, can thrive from the incremental approach. By starting with modest contributions to investment accounts or retirement plans, individuals can leverage the power of compound interest. Moreover, educating oneself about investment strategies can lead to informed decisions, further amplifying the impact of initial contributions. Avoiding debt is equally important; small lifestyle changes that prioritize needs over wants can prevent the accumulation of high-interest loans and credit card debt.

In conclusion, the power of small changes in wealth management cannot be overstated. Implementing minor adjustments to budgeting, saving, investing, and debt avoidance can result in significant financial improvements over time. By adopting these strategies, individuals and families have the opportunity to navigate their financial landscapes successfully, illustrating how the 1% wealth shift begins with small, manageable changes.

Creating a Financial Safety Net: Strategies to Consider

Establishing a robust financial safety net is crucial for protecting oneself against unforeseen events that could adversely impact financial stability. A well-structured financial safety net primarily comprises three key elements: emergency funds, insurance policies, and a diverse investment portfolio. Each of these components plays an integral role in ensuring monetary security and resilience in the face of unpredictable circumstances.

Firstly, creating an emergency fund is one of the most straightforward yet effective strategies. This fund should ideally cover three to six months’ worth of living expenses, providing a financial buffer during periods of unemployment, unexpected medical expenses, or other emergencies. Allocating a portion of monthly income to a dedicated savings account can help accumulate these funds over time. This proactive approach offers peace of mind and serves as a foundational aspect of a comprehensive financial strategy.

In addition to emergency savings, securing appropriate insurance coverage is essential for mitigating financial risks. Various insurance policies, including health, auto, and life insurance, can help shield individuals and families from significant financial burdens. An in-depth review of current insurance needs ensures adequate protection against unforeseen calamities while preventing financial strain when unexpected events arise.

Lastly, diversifying investment portfolios is vital for enhancing overall financial security. By spreading investments across various asset classes—such as stocks, bonds, and real estate—individuals can reduce the impact of market volatility on their financial well-being. This approach not only fosters growth potential but also minimizes risks associated with relying on a single investment type. To assess current situations and implement these strategies effectively, individuals should evaluate their financial goals and tailor their safety nets accordingly.

Long-term Implications of the 1% Wealth Shift on Society

The phenomenon of wealth concentration among the top 1% has far-reaching implications that extend beyond the economic sphere, profoundly affecting societal structures, public policy, and community dynamics. As wealth increasingly becomes consolidated within a small segment of the population, the resultant economic disparities can lead to diminished economic mobility for the majority. This, in turn, can stymie innovation and growth, as less capital circulates in communities that need it most.

The influence of the wealthy elite on public policymaking is another critical area of concern. When financial resources are concentrated, those at the top can wield disproportionate power in shaping legislation, often prioritizing their interests over the broader public’s needs. This can manifest in regressive tax policies, reduced funding for social programs, and a lack of investment in essential public services such as education and healthcare. Inequality in decision-making can perpetuate a cycle where the interests of the many are repeatedly compromised in favor of the few.

Moreover, the societal fabric can become strained under the weight of growing inequality. Communities may experience increased social fragmentation, as economic divides lead to diminished social cohesion. Disparities in wealth often correlate with disparities in access to education and healthcare, exacerbating existing vulnerabilities within marginalized communities. A disengaged populace may further result from feelings of helplessness in the face of systemic inequalities, leading to decreased participation in civic and community activities.

To address these challenges, collective advocacy, awareness initiatives, and meaningful community engagement are essential. Individuals can play a vital role by participating in discussions surrounding wealth equity and advocating for policies that promote inclusivity. Grassroots movements, educational programs, and support for equitable economic practices can aid in counteracting the adverse effects of the wealth concentration, fostering a more equitable society. Future trends hinge on our ability to recognize these issues and take actionable steps towards a shared vision of economic justice.